This strategy anchors the bulk of my portfolio.

It is effortless, boring, yet incredibly effective, and has comfortably netted me a 63% return within 2 years of implementation.

This page will provide a quick run-down on the essence of this strategy.

What are LETFs?

Leveraged Exchange-Traded Funds (LETFs) uses derivatives to multiply the daily returns of an underlying asset or index.

To simplify it, if S&P 500 delivers a 1% return:

•SSO (2x Leverage) would deliver a 2% return.

•SPXL (3x Leverage) would deliver a 3% return.

Conversely, losses are also multiplied.

What is volatility decay?

The general advice is to not hold LETFs over a prolonged period of time due to the concept of volatility decay.

Let’s assume a scenario where we have invested $100 individually into both SP 500 (left column) and SPXL (right column).

Year 1 Results

| Ticker | SP 500 | SPXL (3x Leverage) |

| Initial Investment | $100 | $100 |

| Year 1 Performance | -20% | -60% |

| End of Year 1 Value | $80 | $40 |

Year 2 Results

| Year 2 Performance | +25% | +75% |

| End of Year 2 Value | $100 | $70 |

| Total Outcome | Break Even (0%) | Loss of 30% |

It’s evident that volatility decay demonstrates how LETFs can be problematic or ineffective in downtrends or choppy markets.

Where LETFs work extremely well, however, is during clear uptrends where drawdowns are limited and not a major concern.

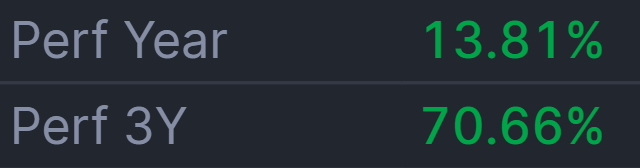

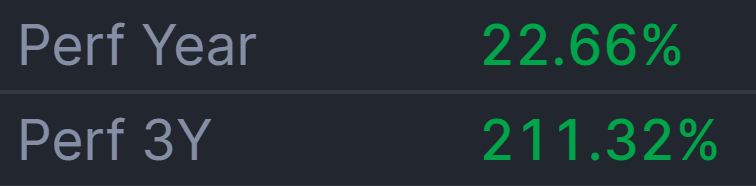

Compare the following YTD gains of SP 500 vs SPXL during an uptrend:

It’s clear that SPXL blows SP 500 right out of the water.

How to discern clear uptrends vs downtrends/chop?

This strategy will demonstrate when we should purchase SPXL and when we should sell SPXL.

Generally, common technical indicators such as MACD, EMAs, SMAs etc. are what we call lagging indicators.

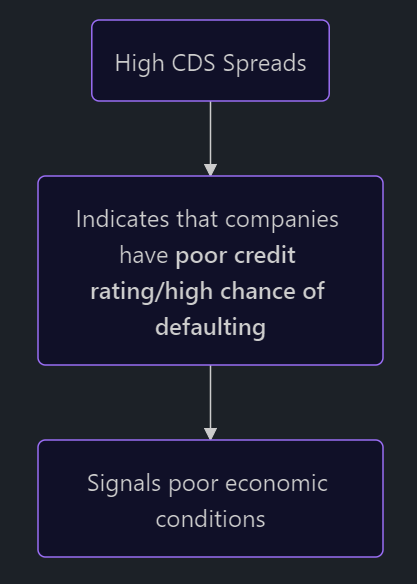

We can instead use a leading indicator that tracks the price of Credit Default Swaps, or CDS for short.

What are credit default swaps?

Let’s take a look at the following scenario:

1. Tan Bank lends $10 million to Huat Trading Co.

2. Tan Bank is worried that Huat Trading Co. might default or go bankrupt.

3. Tan Bank then goes to a third party insurer called Lim Insurance.

4. Tan Bank pays an insurance premium to Lim Insurance to insure their $10 million loan.

5. If Huat Trading Co. defaults, Lim Insurance must pay Tan Bank $10 million.

6. If Huat Trading Co. pays back the loan, Tan Bank makes money from the loan interest but loses the insurance premium paid to Lim Insurance.

The contract between Tan Bank and Lim Insurance is known as a Credit Default Swap, and allows Tan Bank to de-risk their loan.

BAMLH0A0HYM2

BAMLH0A0HYM2 is the name of the ticker used to track CDS Spread (the price of the premium in a CDS contract) in the economy.

It answers the question “Are companies at risk of going broke?”

This means BAMLH0A0HYM2 is more akin to a fundamental indicator of the economy rather than a technical one.

The higher a CDS Spread, the higher the likelihood of companies defaulting. This means that:

• When CDS spreads are low, economic conditions are good and is correlated with an uptrend.

•When CDS spreads is high, economic conditions are poor and is correlated with downtrends/chop.

| CDS | Economic Conditions | Trend |

|---|---|---|

| Falling/Low | Good | Uptrend |

| Rising/High | Poor | Downtrend/Chop |

It’s quite clear that we’d like to invest during periods where CDS is falling or low.

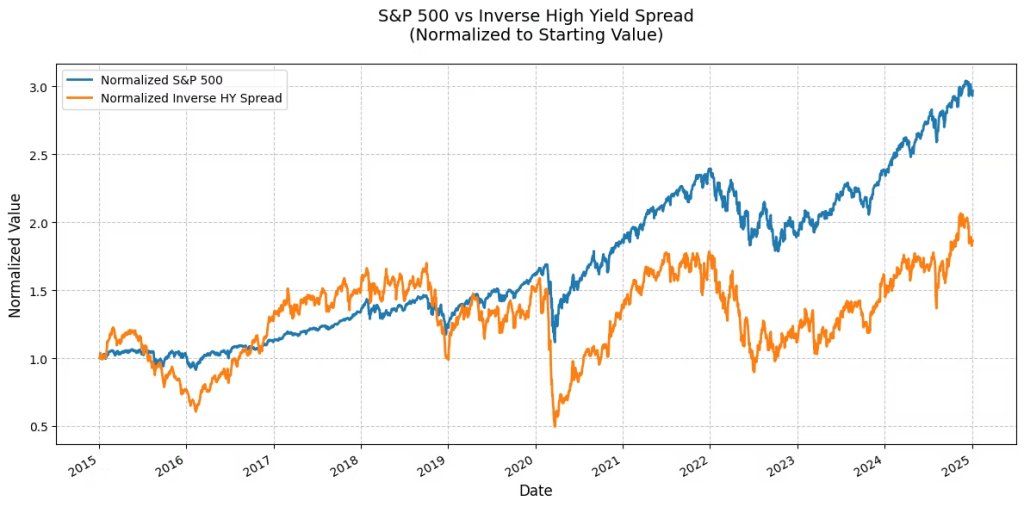

We can see the performance correlation between SP500 and inverse CDS Spreads below.

However, this begs the question – how do we know when exactly have credit spreads risen to the point where it signals an incoming downtrend or choppy market so that we’re able to get out in time?

Trigger Values

I personally use the following entry and exit values:

| Change % in CDS Spreads | Signal | Action |

|---|---|---|

| CDS rises >30% from recent low | Incoming downtrend/chop | Sell SPXL |

| CDS falls >30% from recent high | Incoming uptrend | Buy SPXL |

If we plot these triggers on BAMLH0A0HYM2 into our charting software, it provides us with the dates in which SPXL was in an uptrend.

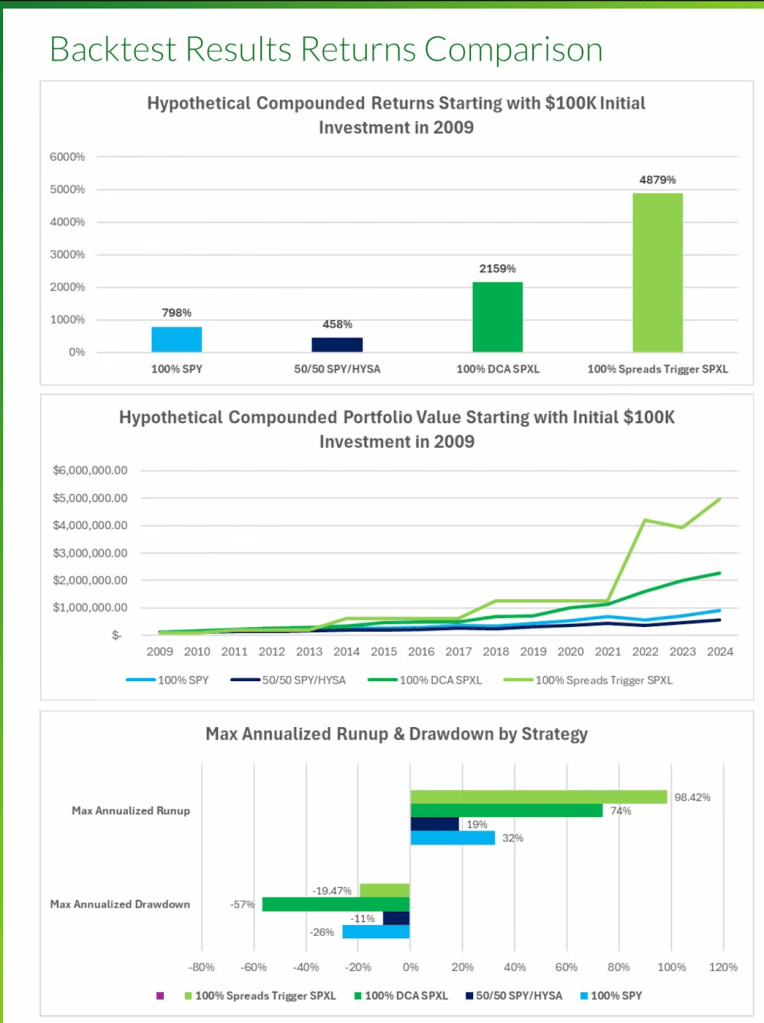

Assuming that our portfolio was entirely invested into SPXL during these uptrends and entirely sold during downtrends/chop, we can plot the following results:

As we can see, this strategy grew our portfolio from an initial amount of $100k into approx. $5 million over a 15 year period.

It also provides the largest annualized runup while also maintaining an annualized drawdown lower than just holding SP500.

Alternate Trigger Values

As previously mentioned, my own personal entry and exit values are +30 Exit/-30 Entry.

You’re free to adjust your entry and exit values based on your desired CAGR and max drawdown. Generally, lower values reduce both drawdowns and returns.

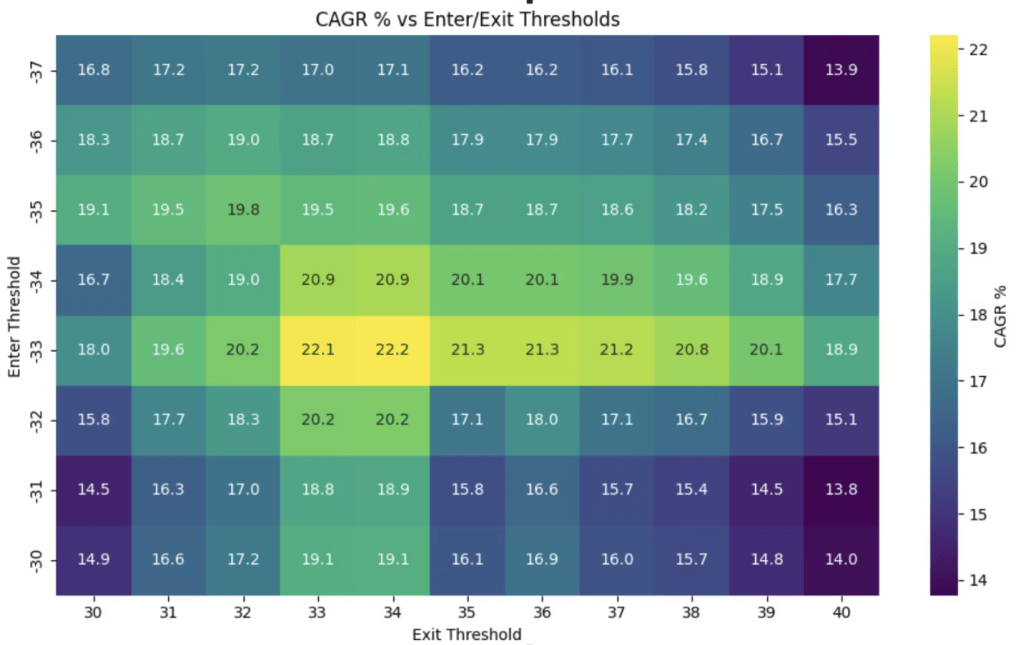

Here is a comparison of different trigger values back tested from 2003.

+30 Exit/+30 Entry

+40 Exit/-35 Entry

+30 Exit/-35 Entry

CAGR Comparison

The values -33/+34 seems to yield the highest CAGR % overall.

Regardless of the trigger values chosen, the CAGR of this strategy still outperforms SP 500’s CAGR of 8.38% (2003 – 2024; adjusted for inflation)

In addition, we have also managed to avoid the massive market crash that occurred during the GFC (-56.8%) and the Covid-19 pandemic (-33.8%) in every dataset.

If the volatility or drawdown of SPXL is too much to handle, I would suggest swapping over to SSO for 2x Leverage instead.

Impact of DCA on strategy performance

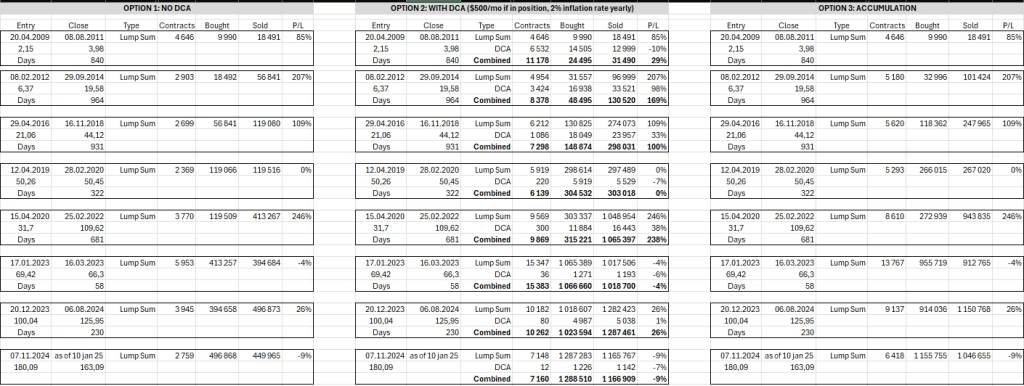

Presume a principal amount of $10,000, beginning from 2009.

Results

Option 1 (No DCA): $450k

Option 2 (DCA during uptrend): ~$1 Million

Option 3 (Lump sum in beginning of next uptrend): ~$1 Million

There are no significant difference between Option 2 vs Option 3, however the concept of DCA significantly affects the return in comparison to Option 1.

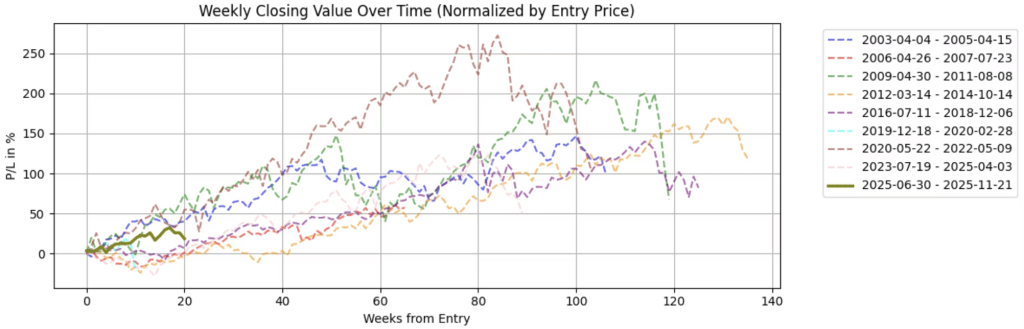

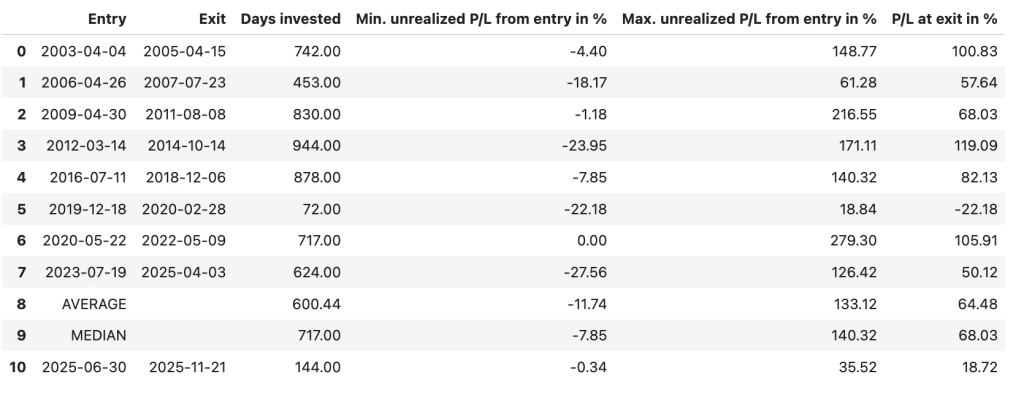

Expectations of each trade

The x-axis shows the number of weeks from entry date, while the y-axis shows the P&L %.

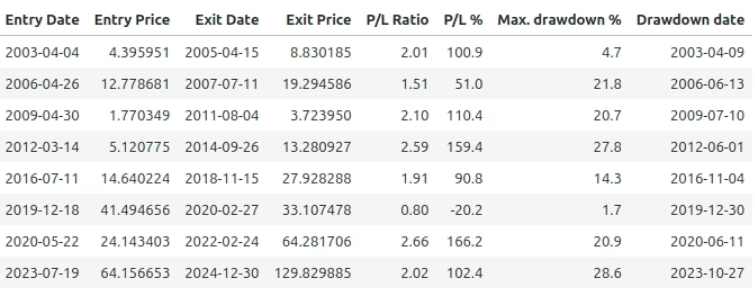

The median trade lasts approx. 2 years at 717 days. In other words, you’re expected to passively hold SPXL for a period of ~2 years.

An average of -11.74% drawdowns below the entry price is normal, especially within the first 20 weeks.

The average realized P&L at exit dates are +64.48%, far below the max. unrealized P&L of 133.12%. The exit always comes after the top, which makes sense, as otherwise you would sell too early every time.

Exit Periods

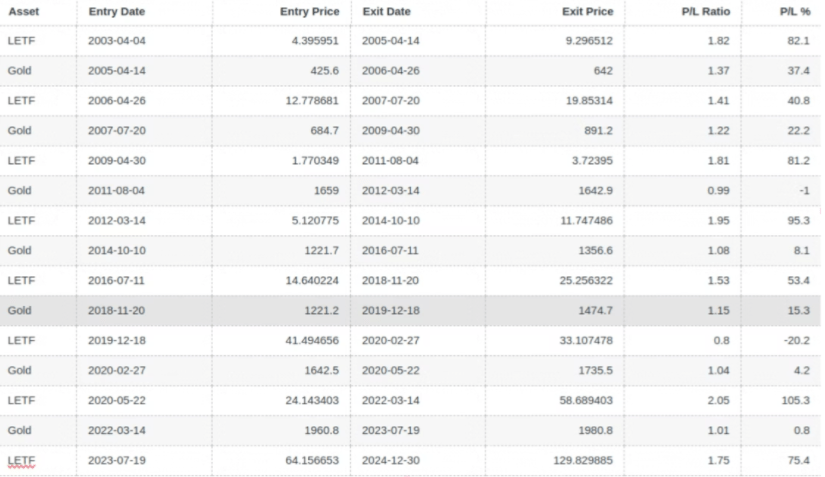

While divested from SPXL during exit periods, let’s explore which asset is optimal to park our cash in.

Ideally, it should have low correlation to SP500’s performance.

GLD, ZROZ, and TLT appears to be the most consistent performers during the exit periods, offering potential gains over just holding cash.

My preference would be GLD due to its status as a traditional safe-haven asset.

Simulating 100% SPXL during entry periods and 100% GLD during exit periods gives us the following results:

Of course, you’re free to approach each exit period differently as there’s no one-size-fits-all solution.