Supply Side

Copper is currently facing a supply shortage.

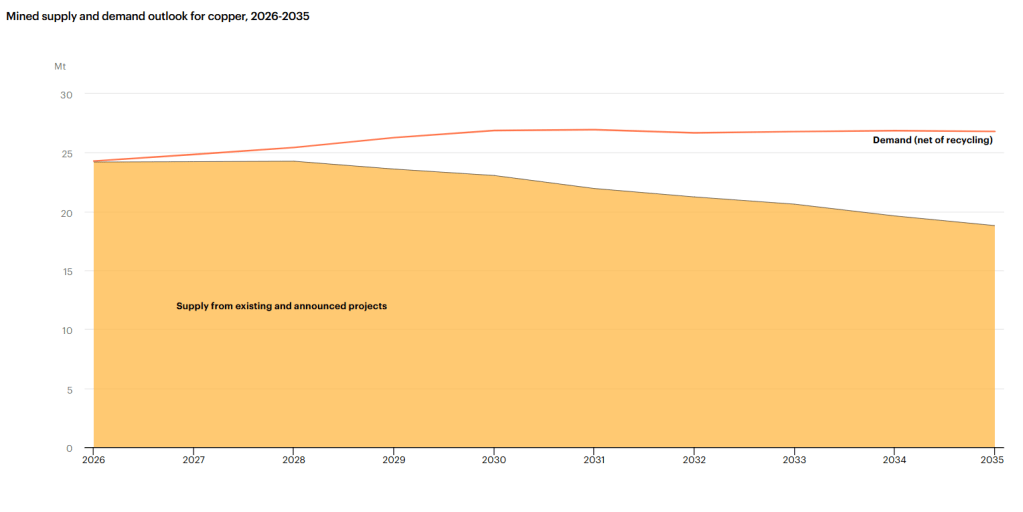

The International Energy Agency has projected that copper is set to face a major deficit of 30% by 2035.

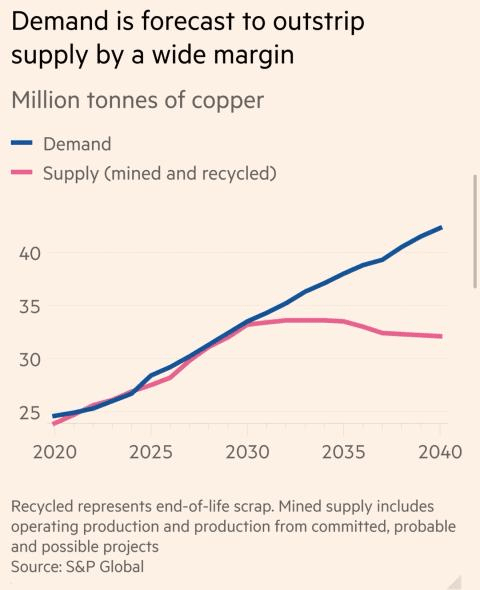

S&P Global has forecasted demand is on track to exceed supply by a huge margin.

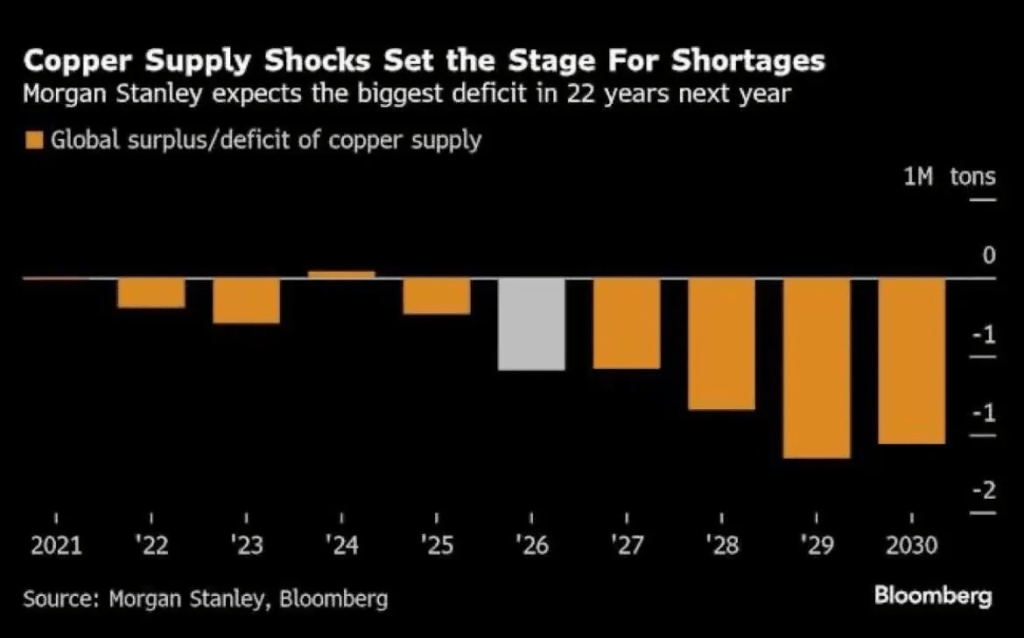

Research by Morgan Stanley has shown that copper is expected for its biggest deficit in 2026 and set to widen even further.

JP Morgan has also forecasted copper prices to increase due to growing demand and supply shortages.

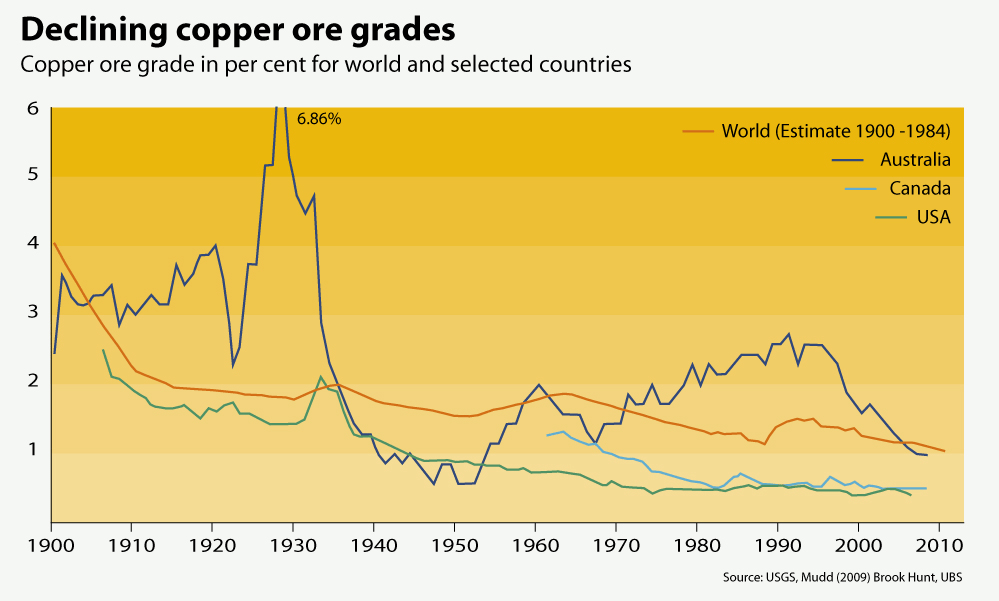

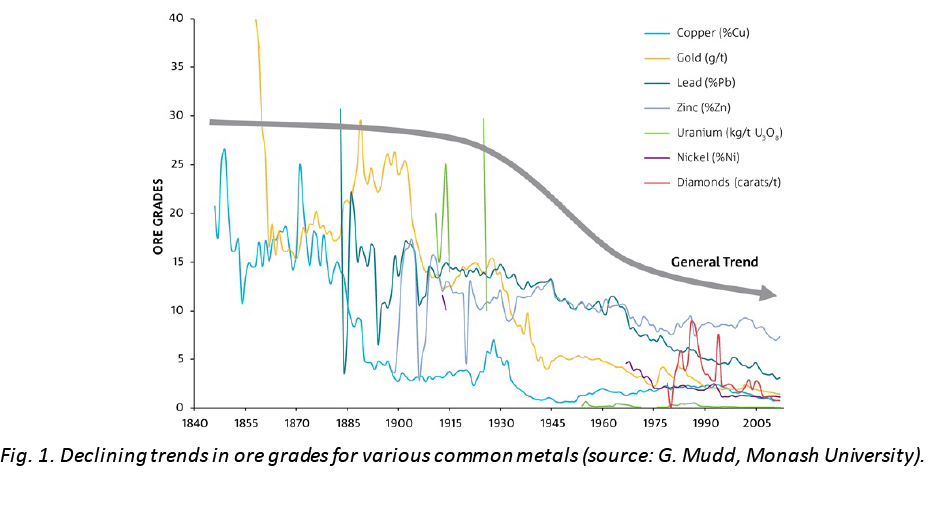

In addition, copper ore grades are also diminishing.

Global copper ore grades have fallen roughly 40-50% since 1990s, meaning miners have to dig up significantly more rock just to produce the same amount of refined copper.

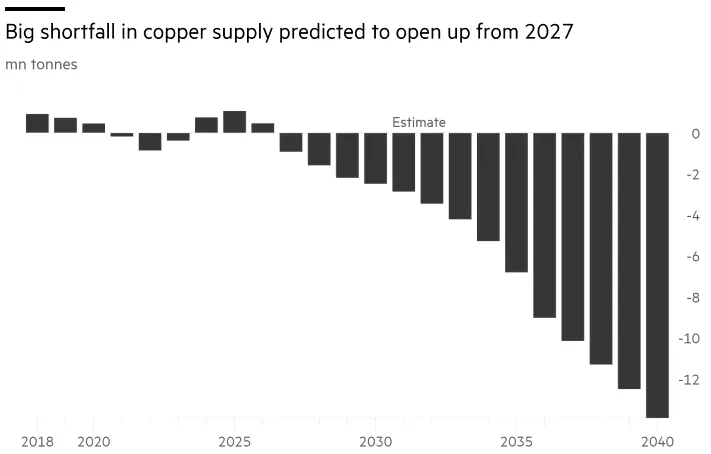

The message is abundantly clear: copper is facing a major deficit.

So why not increase supply by building more mines?

It takes roughly 10-15 years to develop a copper mine from discovery to production.

To meet demand for 2030, the mining industry needed to deploy enough capital a decade ago to get the mines up and running on time.

However, Wood Mackenzie estimates that total copper-mining investment over the past six years reached only about $76 billion. For context, it’s estimated that over $200 billion in new investment is required to bridge the gap between demand and supply.

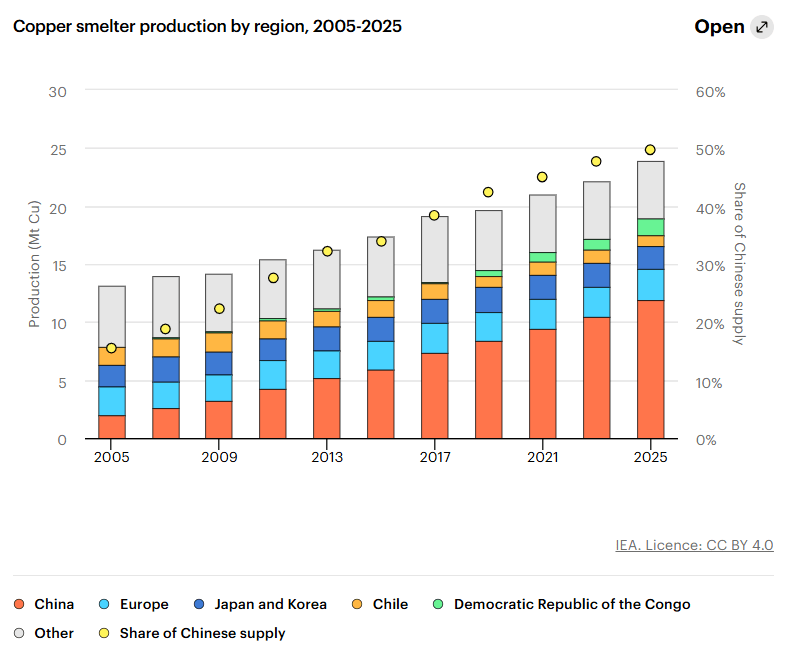

Over the last decade, copper smelter production has expanded but the mines have not kept up.

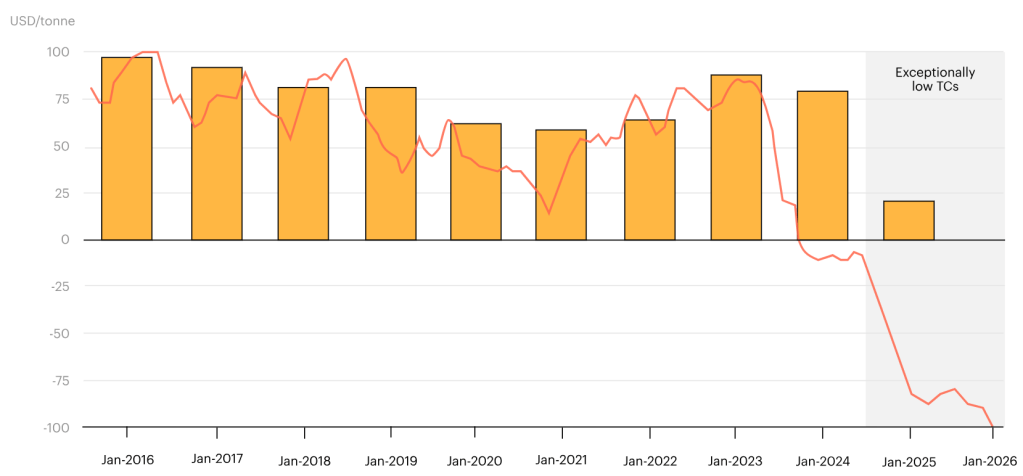

In fact, the shortfall of copper mines has resulted in a bidding war between copper smelters.

TR/RCs are fees that miners pay smelters to process their ore. The spot rates for TR/RCs have actually gone negative, meaning smelters are paying the miners to smelt their ores.

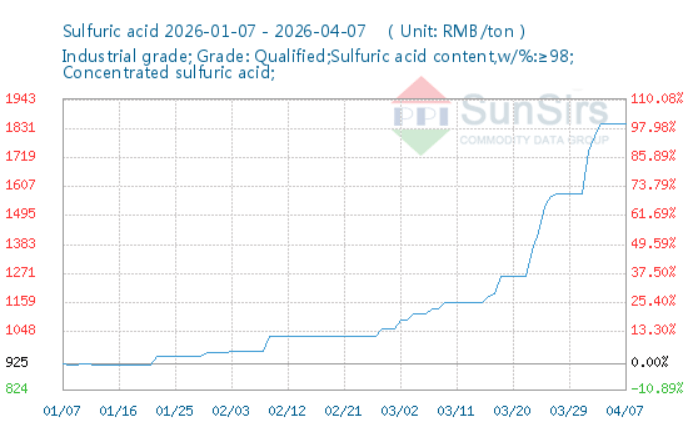

A byproduct of smelting copper ore concentrate is sulfuric acid. Smelters produce approx. one ton of sulfuric acid from one ton of copper ore concentrate.

In Q1 2026, TR/RC spot rates are approx. -$100 per mt. Smelters are currently selling sulfuric acid to offset the negative spot rates, which is priced at ~1800 RMB per mt or ~$260 per mt.

As the copper shortage continues, we can expect sulfuric acid prices to rise in tandem.

Demand Side

Let’s now take a look at the demand drivers that is currently driving up copper.

The growth of the AI industry is the primary catalyst that is driving copper demand. The AI industry relies on two highly copper-intensive necessities:

- Expanding data centers to build the physical infrastructure needed to compute and scale AI

- Rewiring and modernization of the power grid to deliver enough electricity to these data centers

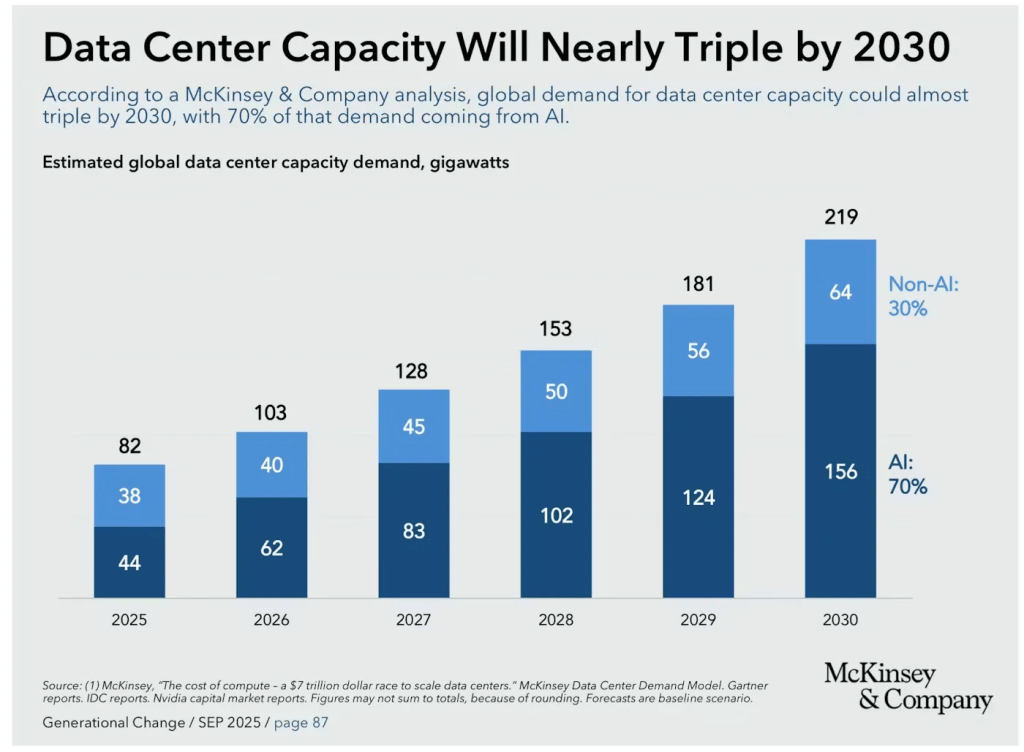

We can see that data centers for AI continue to scale up globally, according to a McKinsey Analysis.

Advanced data centers are exceptionally copper-intensive, requiring high-density wiring, liquid cooling systems, and massive electrical infrastructure to handle extreme power loads. A single facility can contain tens of thousands of miles of copper.

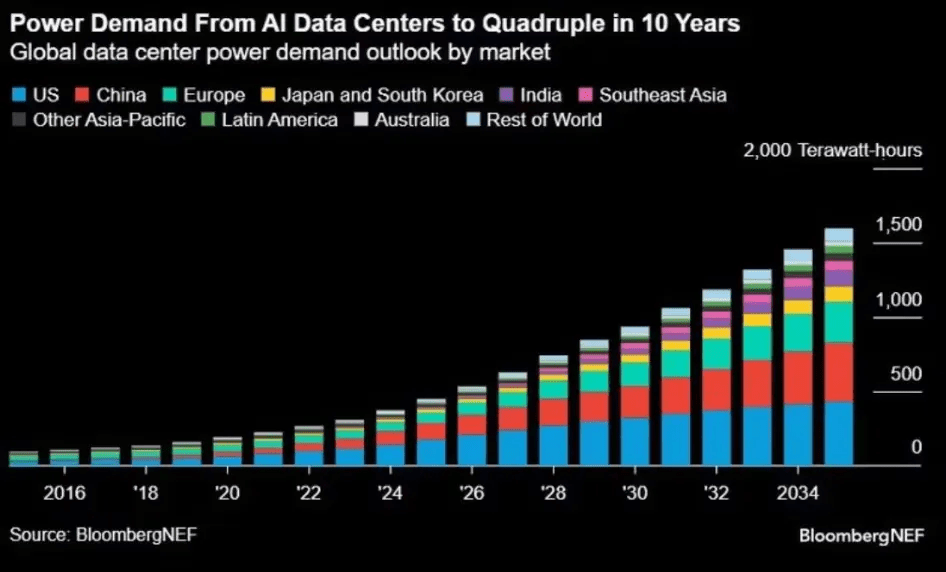

With the expansion of data centers, power demand is projected to quadruple over the next 10 years.

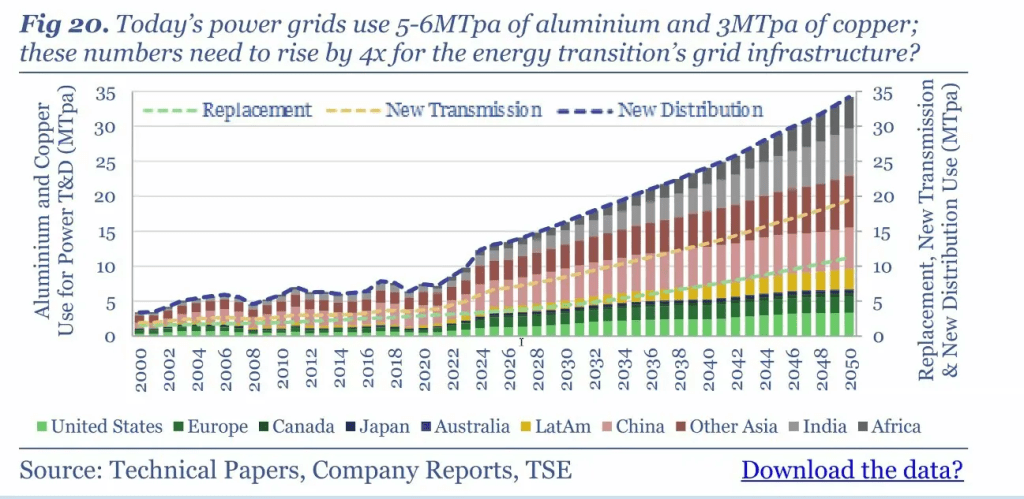

The existing electrical grid is unable to handle the current power demand required. The modernization of the electric grid requires 4x the current copper usage to meet power demands.

Technicals

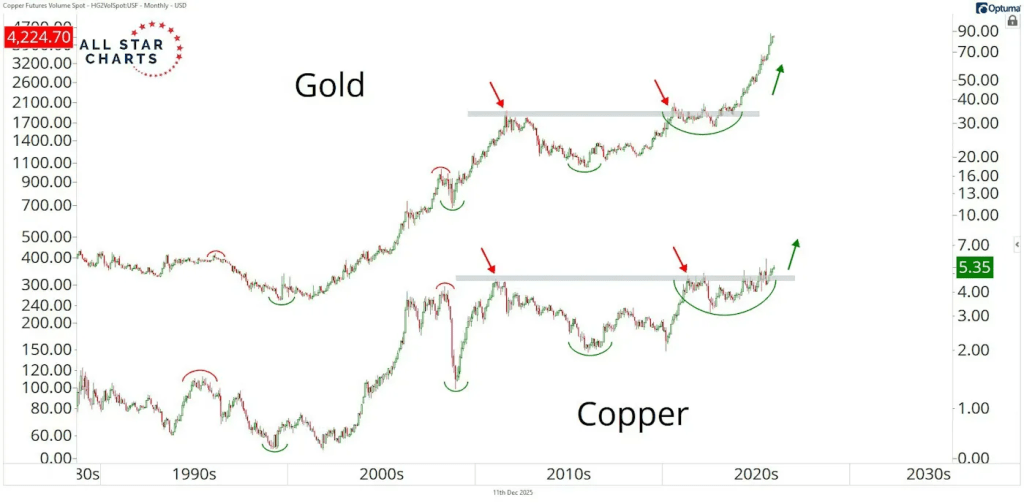

If we take a look at the performance of gold after it broke out of its multi-year resistance, we see that gold has risen over 100%. Furthermore, gold is backed by a fundamental narrative due to dollar debasement and increasing global uncertainty.

Currently, copper is beginning to break out of its multi-year resistance. Copper also possesses a strong fundamental narrative to justify its rally towards higher prices.

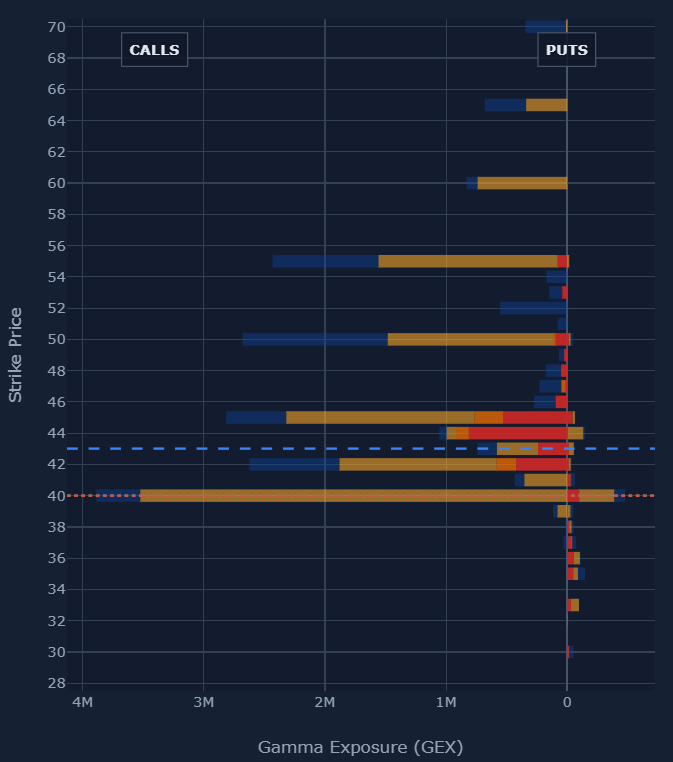

Let’s take a look at the GEX chart for COPJ, whose ETF provides us a higher exposure to the copper market. With a 1y DTE, we can see that there’s a bullish outlook leaning heavily towards calls.

We can expect prices of COPJ to be extremely supportive at $40.

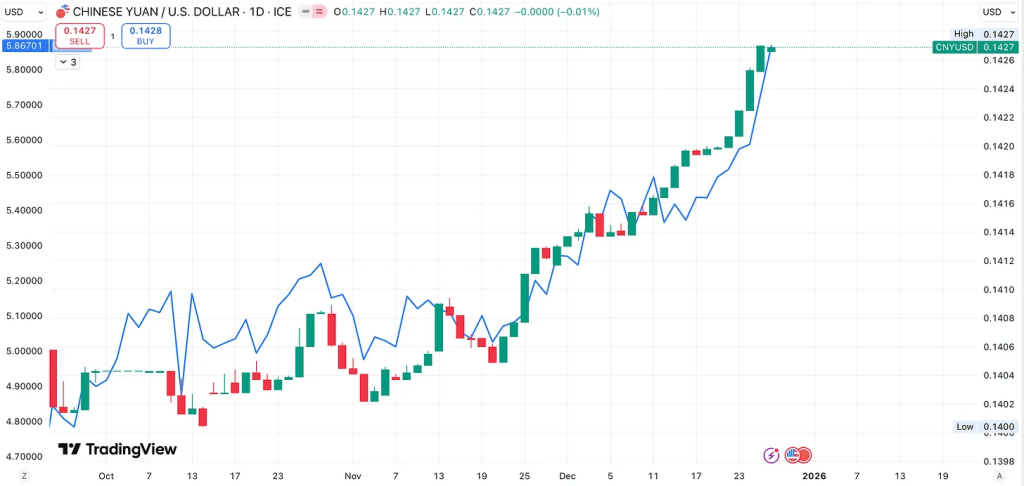

Copper also exhibits a positive correlation with CNY as China roughly accounts for 50% of global demand.

Goldman Sachs’ 2026 FX strategy has estimated that the CNY is trading roughly 25% below its fair fundamental value against the U.S. dollar. The bank’s research team explicitly stated that CNY exposure was one of its “highest-conviction” foreign exchange trades for 2026.

As CNY strengthens towards the 25% FVG, the purchasing power of Chinese buyers surges as a stronger CNY makes it cheaper to import copper.

This incentivizes Chinese buyers to frontload and stockpile copper to hedge against future tightening supply, which will likely drive up copper prices even higher.

Overall, assuming the AI industry continues on its current trajectory, copper displays a strong fundamental narrative for a long-term investment.